The All in One Loan

Product Highlight: The All in One Loan

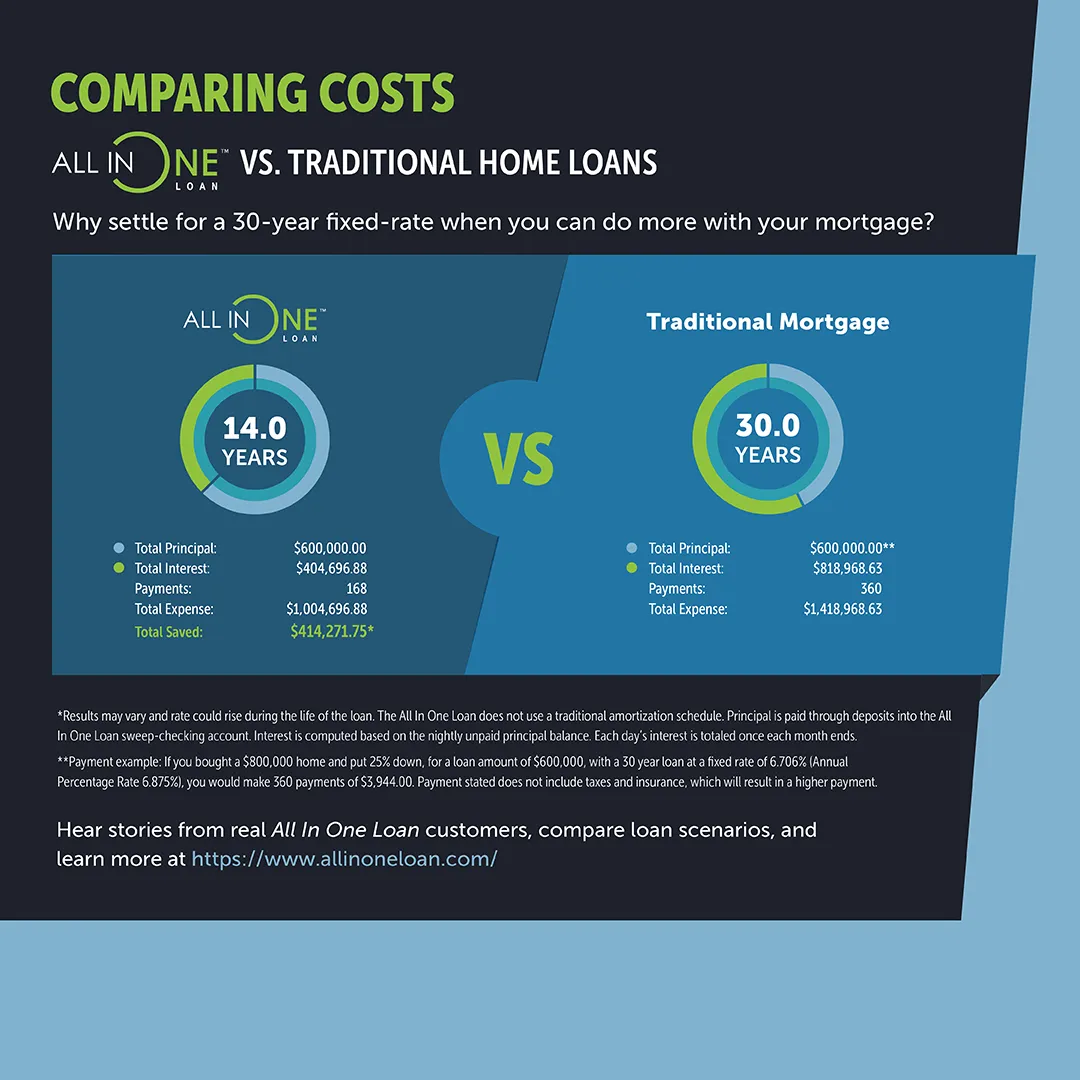

Would you like to reduce your mortgage interest costs and potentially pay off your home loan years earlier than planned? For the right borrower, an innovative mortgage product called the All in One Loan can help accomplish exactly that.

So what makes the All in One Loan different?

Imagine if, instead of paying interest on your full mortgage balance every month, you could temporarily reduce that balance simply by keeping your cash in a linked account. That is the core advantage of the All in One Loan.

How Does It Work?

The All in One Loan combines a mortgage with a linked checking account. All deposits are applied directly to loan principle which lowers the outstanding daily balance through which interest is computed.

For example, when a borrower deposits their paycheck into the linked checking account, the mortgage balance is immediately offset by that deposit. As funds are used throughout the month for regular expenses, the checking account balance decreases, and the effective mortgage balance gradually increases again.

This structure allows borrowers to put their income to work more efficiently. Their cash helps reduce mortgage interest costs while it sits in the account, yet the funds remain fully accessible at any time.

If the borrower continues making the same monthly payment they would make on a traditional mortgage, more of each payment is applied toward principal because less interest accrues over time. The result can be substantial interest savings, faster mortgage payoff, and greater flexibility in accessing home equity.

Who Is It Best For?

The All in One Loan is not the right fit for every borrower. It works best for clients with strong cash flow, significant liquid assets, or the ability to make large recurring deposits into the linked account.

It is also an excellent solution for financially savvy clients looking for more strategic ways to utilize their home equity for investments, college planning, retirement strategies, or other long-term financial goals.

Recently, I spoke with a client whose private bank offered an extremely competitive adjustable-rate mortgage due to the size of their investment portfolio. At first glance, the lower ARM rate appeared to be the obvious choice. However, because the client had substantial monthly cash flow and strong financial discipline, the All in One Loan became a compelling alternative.

Even compared to the lower introductory ARM rate, the projected long-term interest expense with the All in One Loan was significantly lower — and the projected payoff timeline was less than half that of a traditional mortgage.

For borrowers who want to make their money work smarter, not just harder, this is a powerful option worth exploring.

If you would like to learn more about the All in One Loan, give me a call.